The 2023/2024 tax season is not that far away. For employers and workers alike, the year-end tax adjustment is an important procedure. It is mandatory, in order to “square up” the correct taxes owing. For most employees, it also puts more money in their pocket by including more allowable tax deductions than the employer includes during the regular payroll cycle. These useful online resources for Japanese year-end deductions make it easier for everyone, including Sharoushi, accountants, employers, and of course, the employees, all of whom may be involved in tax reporting.

On Japan’s National Tax Agency (NTA) tax portal, the following notice is made:

- The year-end adjustment for Reiwa 5 will be the same procedure as last year (Reiwa 4).

- We have published a “leaflet” with various information on year-end adjustments for those who are obliged to withhold tax.

- For the calculation of the year-end adjustment using the withholding book, you can efficiently calculate the tax amount of the year-end adjustment by using the “Year-end adjustment calculation sheet” (Excel).

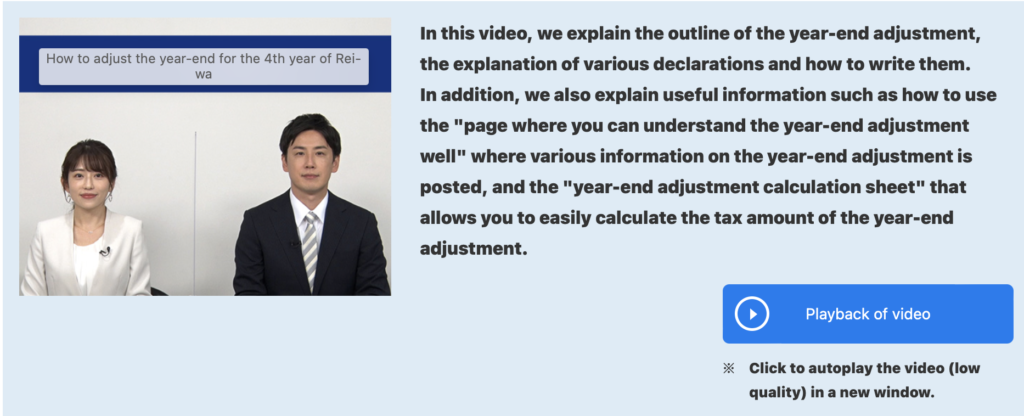

The NTA also notes that, again this year, there will be no live events, seminars, etc. The resources include interactive fillable forms that will make calculations for the user. NOTE: All materials are in Japanese. There are chatbots for greater interaction, as well as videos, PDFs and EXCEL documents. The starting point to access all the resources is here.

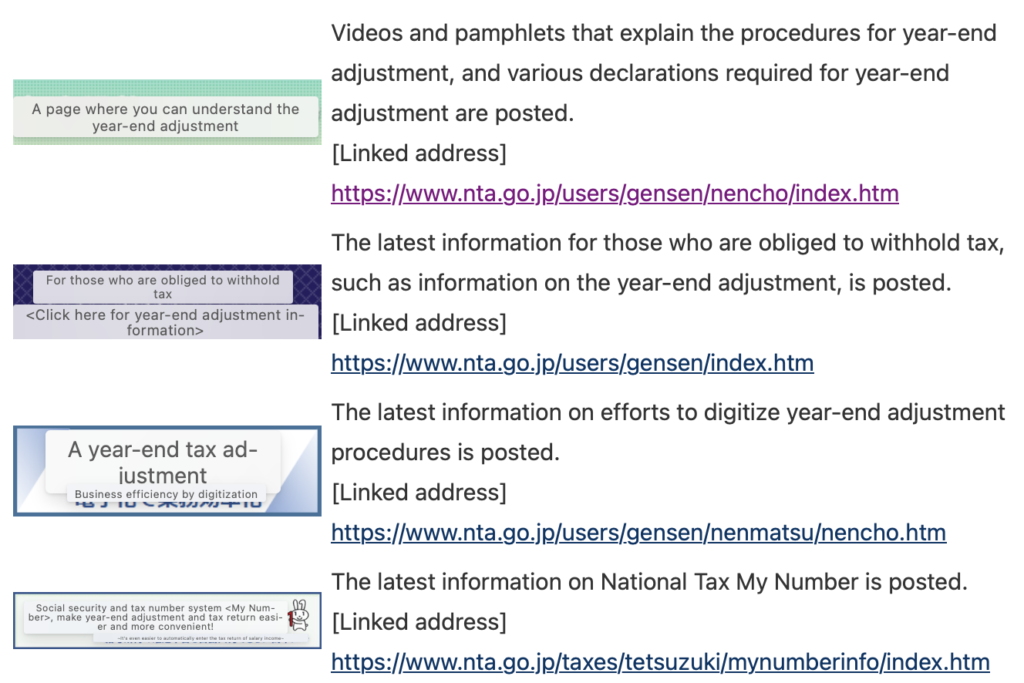

Screen Shots From the Portal.

Some Year-End Deduction Highlights Regarding Non-Residents.

(1) From January 2023, dependent relatives who are non-residents who are eligible for dependent deductions include the following people.

a. People between 16 and 30 years old

b. People over 70 years old

c. Among people between the ages of 30 and 70, those who fall under any of the following

(i) A person who no longer has an address or residence in the country due to studying abroad

(ii) Disabled people

(iii) Those who have received more than 380,000 yen in payment from income earners who want to receive the application of the dependent deduction for living expenses or education expenses in that year.

(2) In the year-end adjustment, if a dependent relative who is a non-resident who intends to apply for the dependent deduction falls under (1) above, it is necessary to submit or present the confirmation document related to the dependent relative to the payer of the salary.

Verse Corporation publishes articles on timely issues in Japanese Social Welfare and Labour Law. Japanese payroll, source deductions, and all labor law work & pay rules regarding compensation, social insurance, absenteeism & sick leave, etc. require strict adherence. Labor/employment law can be complex, even for Japanese companies, and must be handled mostly in Japanese. As with all social welfare and labor law matters in Japan, please seek out professional Sharoushi (Certified Labour Law and Social Insurance Attorney.)

Verse and other qualified Labor Law Attorneys (Sharoushi) are capable of guiding your company or your supporting professionals through this process. These useful online resources for Japanese year-end deductions will come in handy.